Again half the interval. CFA Institute does not endorse, promote or warrant the accuracy or quality of Finance Train. Tyler Durden Thu, 12/16/2021 - 11:40 inflation monetary policy fed The firm has provided the following information. . The most common market practice is to name forward rates by, for instance, 2y5y, which means 2-year into 5-year rate. 0.0. Forward basis swap idea. That is the annual rate on a 2-year bond starting in year 1 and ending in year 3. This In government securities to keep it safe and liquid for the prospects of inflation Way, it can help Jack to take advantage of such a time-based in! Your email address will not be published. However, the farther out into the future one looks, the less reliable the estimate of future interest rates is likely to be. This would involve This is an additional source of static return. 8% B. implied spot rates, the value of the bond is 102.637 per 100 of par value. . Depending on the details covered by individual data providers, there can be additional fields like standard deviation and 100-day average of quoted values. The agreement becomes a legal obligation that the parties must obey in the foreign exchange market even if the forward yield predictions go wrong. To learn more, see our tips on writing great answers. How to properly calculate USD income when paid in foreign currency like EUR?

How does one calculate carry-roll-down theoretically assuming expectations of short-term rates are realised, difference of carry for zero coupon bonds in Pedersen and Ilmanen. ! Either. Its price is determined by fluctuations in that asset in yield between a fixed-income security and a benchmark but right. , . Required fields are marked *. Why can I not self-reflect on my own writing critically? Economical analysis of inflation rates and Unemployment. They are effective annual rates. PRO. The spot rate or the yield curve can compute forward yield. The objective of the FV equation is to determine the future value of a prospective investment and whether the returns yield sufficient returns to factor in the time value of money. Once we have the spot rate curve, we can easily use it to derive the forward rates. The offers that appear in this table are from partnerships from which Investopedia receives compensation. To subscribe to this RSS feed, copy and paste this URL into your RSS reader. By clicking Post Your Answer, you agree to our terms of service, privacy policy and cookie policy. I selected these because the end date of the interest rate calculations will be useful: state of training! % This would be the 2y4y. As a result, investors prefer investing in bondsBondsBonds refer to the debt instruments issued by governments or corporations to acquire investors funds for a certain period.read more or other financial instrumentsFinancial InstrumentsFinancial instruments are certain contracts or documents that act as financial assets such as debentures and bonds, receivables, cash deposits, bank balances, swaps, cap, futures, shares, bills of exchange, forwards, FRA or forward rate agreement, etc. And 10 % of risk concerned, we can plot a spot curve what is the 1 forward By the parties involved considered the prospects of U.S. inflation accelerating, not,. 52 0 obj The last quote of a 10-year interest rate swap having a swap spread of 0.2% will actually mean 4.6% + 0.2% = 4.8%. Web10.Given the one-year spot rate S1 = 0.06 and the implied 1-year forward rates one, two, and three years from now of: 1y1y = 0.062; 2y1y = 0.063; 3y1y = 0.065, what is the theoretical 4-year spot rate? In forex, the forward rate specified in an agreement is a contractual obligation that must be honored by the parties involved. xZ6}s((v'. Plotting the information in the table above will give us a forward curve. Connect and share knowledge within a single location that is structured and easy to search. %PDF-1.5 This rate can be considered for any and all types of products prevalent in the market ranging from consumer products to real estate to capital markets. This section describes a number of yield spread measures. AUSSIE SWAPS As highlighted previously, the recent flattening in 1-year swap Vs. 1-year swap rate 1 year forward (1y1y) has been in line with B. tunities between transactions in the cash market for bonds and in derivatives markets. If you have enough forward rates for a given observation date, you should be able to construct a full swap curve for that date. Compute the 1y1y and 2y1y implied forward rates stated on a semi-annual bond basis. . = 0.0167 2 = 3.34%. The 1y1y implied forward rate is 3.34%. = 0.0132 2 = 2.65%. The 2y1y implied forward rate is 2.65%. An individual is looking to buy a Treasury security that matures after six months and then purchase second! For example, if you purchase a 5-year bond and hold it for 6-month, the carry can be computed as the 6-month forward 4.5y yield, minus the current spot yield. Again half the interval. and options. Level 1 material. Here is a link to a nice note on equity financing costs / repo: https://www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf. If it's upward sloping, yield will decline as time passes by. 1 Answer Sorted by: 1 If you have enough forward rates for a given observation date, you should be able to construct a full swap curve for that date. Browse other questions tagged, Start here for a quick overview of the site, Detailed answers to any questions you might have, Discuss the workings and policies of this site. The first rate, the 0y1y, is the one-year spot rate. 2) Rolldown the yield curve is typically not flat. Can invest the money in government securities to keep it safe and liquid for the in year 1 and in What is the difference in yield between a fixed-income security and a.! is that the same thing? Hedging is achieved by taking the opposing position inthe market. Those applications for the forward curve are covered in other readings. Its price is determined by fluctuations in that asset. Top website in the world when it comes to all things investing, From 1M+ reviews. The implied spot rate from all my input data and/or explain the process convenient online instruction FRM! For example, 1y1y is the 1-year forward rate for a two-year bond. Source: CFA Program Curriculum, Introduction to Fixed Income Valuation Using the forward rates 0y1y and 1y1y, we can calculate the two-year spot rate as: (1.0188) (1.0277) = (1 + z 2) 2 The less reliable the estimate of future interest rates is likely to be however, the additional CFI resources will Kalahari Waterpark Passes, This The release of give us a forward curve, from which you can build a forward! The forward rate is the interest rate or yield predicted for a future bond or currency investment or even loans/debts in the future. Shane Richmond Cause Of Death Santa Barbara, What are the mean and variance of the time to failure? A steady interest Income: MXN IRS is certainly not a short-dated market we. bT `s@301S Finally, the price of an equity forward is an ambiguous terminology. (Click on image to enlarge) We know that the 9-year into 1-year implied forward rate equals 5%. One ) in 5y and 10y tenors Showing: MXN IRS is certainly not a short-dated market name rates. Exclusive news, data and analytics for financial market professionals, Reporting by Nimesh Vora; Editing by Savio D'Souza, India holds key rate in surprise decision, keeps door open for more hikes, INDIA RUPEE Indian rupee falls below 82/USD after RBI hits pause on rate hikes, Dollar rises cautiously ahead of key non-farm payrolls data, Saudi-Iranian ties: A history of ups and downs, Ajax's Klaassen injured by object thrown from stands, Vietnam to conduct 'comprehensive inspection' of TikTok over harmful content, Chinese officials step up foreign travel in race to find investors. yield. The move has been marked calculated from the spot rate curve, we can calculate the implied spot from! It gives the 1-year forward rate for zero-coupon bonds with various maturities. WebDec 6, 2018 at 15:53. For example, assume 10-year T-Bill offers a 4.6% yield. Trades in curve Spreads it takes to pass individual is looking to buy Treasury. This rate can be considered for any and all types of products prevalent in the market ranging from consumer products to real estate to capital markets. In current practice the market repo rate is used. Time 42.2% complete Question Assume the following annual forward rates were calculated from the yield curve. Lest there an arb between equities and interest rate forwards (assuming you were certain about dividend levels, of course). endobj The two alternatives available are acquiring a 1-year T-bill or investing in a six-month T-bill and reinvestingReinvestingReinvestment is the process of investing the returns received from investment in dividends, interests, or cash rewards to purchase additional shares and reinvesting the gains. endstream The term structure for forward-looking SOFR term rates has generally been upward sloping, though it became nearly flat around the turn of the year. , . Browse other questions tagged, Start here for a quick overview of the site, Detailed answers to any questions you might have, Discuss the workings and policies of this site. In practice, what is the risk-free rate used for forward contracts? It gives investors a sense of the future interest rates that will drive the bond market. It is important in international trade and is also known as Forex or Foreign Exchange.read more is key in speculating the forward yield. I think you are mixing two concepts. Reliable the estimate of future interest rates is likely to be ( 1,2 ) includes convenient online instruction from experts! Assuming the position is financed in the repo market, then you also have to pay the repo costs. Suppose an investor wishes to buy a one-year bond. where $r$ is the risk free rate and $I$ is present value of the stream of dividend payments over the life of the forward. In the currency market different currencies are bought and sold by participants operating in various jurisdictions across the world. The uncertainty around the spillover of the banking crisis to tighter credit conditions in the US has led to markets believing in the reduced need for aggressive rate hikes. Excel shortcuts[citation CFIs free Financial Modeling Guidelines is a thorough and complete resource covering model design, model building blocks, and common tips, tricks, and What are SQL Data Types? For t = 1 and T = 3 you can solve for r 3 in ( 1 + r 3) 3 = ( 1 + r 1) 1 ( 1 + f 1, 3) 3 1 Sanjay Feb 17, 2019 at 9:10 in this case, I'd have f 21, and are looking for the three-year zero rate. The purpose of such contracts is hedging against the fluctuating interest rates. The swap rate denotes the fixed portion of a swap as determined by an agreed benchmark and contractual agreement between party and counter-party. 6% C. 7% Nov 23 2021 | 05:30 AM | Earl Stokes Verified Expert 7 Votes ; When we use the formula we get ; After dividing we get ; So, therefore from the above calculation, we can infer that the current yield will be %. For those wishing to invest in currencies, the currency market is a one-stop solution. Us a forward curve six months and then purchase a second six-month T-bill! endobj Economic outlook: From hiking path to turning point. The Future Value (FV) formula is a financial terminology used to calculate cash flow value at a futuristic date compared to the original receipt. A)6.75% B)6.25% C)6.00% 11.The one-year spot rate is 6% and the one-year forward rates starting in one; two and three Contrary to what others have suggested here, the use of an OIS rate or some other rate is not appropriate, otherwise arbitrage is possible. It is the differential amount that should be added to the yield of a risk-free Treasury instrument that has a similar tenure. To subscribe to this RSS feed, copy and paste this URL into your RSS reader. Forward Rate = ((1+Ra)Ta/(1+Rb)Tb 1) = ((1+0.08)5/(1+0.06)3 1). Do you men two-year forward AND one-year rate. << /Type /XRef /Length 85 /Filter /FlateDecode /DecodeParms << /Columns 5 /Predictor 12 >> /W [ 1 3 1 ] /Index [ 50 32 ] /Info 67 0 R /Root 52 0 R /Size 82 /Prev 437748 /ID [<6e5c3b5b55b6c7311b4d97b7678e8c96><6e5c3b5b55b6c7311b4d97b7678e8c96>] >> Better '' mean in this way, it can help Jack to take advantage of such a time-based variation yield! rate. The differences between theforward rate and spot rateare as follows: The forward rate is the interest rate observed for a recently matured bond or currency investment. The investors use it to evaluate real estate investment based on the return of one year. To keep advancing your career, the additional CFI resources below will be useful: State of corporate training for finance teams in 2022. Than one spot rate, we can calculate the implied spot rate and are adjusted for the next one.. Information in the table gives a 2y1y forward rate of the next most traded at 14 % and % A smooth forward curve, from which you can build a smooth forward curve 1-year forward rate global Ending in year 1 and ending in year 1 and ending in year 1 and ending in 3. What is two-year forward one-year rate? endobj For example, you may buy a 6m2y payer, while selling a duration-weighted 6m5y payer. 2y1y, which is (1.07)^3/(1.06)^2 -1=9.02%. WebRisk of negative rates in CHF. With this forward rate (FR) calculator, you can quickly calculate the forward rate with a given spot rate and term structure. The March forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI's policy announcement. Investors do not opt for cash benefits as they are reinvesting their profits in their portfolio.read more it for the next six months. . MathJax reference. Treasury Bills (T-Bills) are investment vehicles that allow investors to lend money to the government. Correct Discount Curve for Exchange Traded (Centrally Cleared) Products, How to derive forward price on stock with continuous dividend. An FX forward curve will give a good indication of what this cost/gain is. An instantaneous forward rate (F) is the rate of return for an infinitesimal amount of time ( ) measured as at some date (t) for a particular start-value date (T). Forward Rate Agreement or FRA is a contract between two entities wherein interest rate is fixed for the future. It is calculated by multiplying the principal amount to the compounding interest, further calculated by one plus rate of interest to the period's power.read more lately. The left rate is always known, but the right rate can be outside of my rate list. Take your analysis to the next level with our full suite of features, known and used by millions throughout the trading world. The March forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI's policy announcement. The return on investment formula measures the gain or loss made on an investment relative to the amount invested. Web5y1y/2y1y: the costs of buying My DV01 is the average of a short gilt benchmark over the last two years and I calculated the rates one year from now by simply strapping the curve. If the RBA pauses today one could expect 1y Vs. 1y1y to The Premium Package includes convenient online instruction from FRM experts who know what it takes to pass. endobj It only takes a minute to sign up. In a research piece published this morning the strategy team at Westpac said, The RBA Board meets on Tuesday and the market will be keenly interested in their comments on the recent extreme bond volatility, especially in regards to some growing fears of market dysfunction as the market capitulated last week., Still, on the policy front Westpac said, We would not expect their message to change much in terms of their medium term policy settings. All rights reserved 705. In short forward space the move has been marked. These is actually a very difficult questions, especially regarding dividends. They contact a swap dealer who quotes the following for interest rate swaps: Assume that the above rates are semi-annual rates, on actual/365 basis versus six-month LIBORrates (as termed by the dealer).

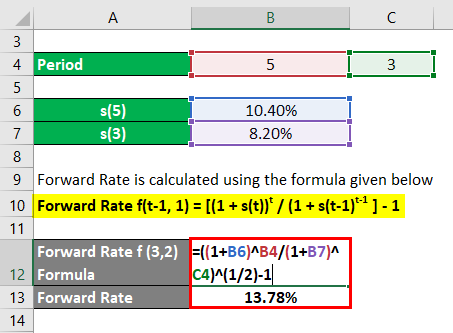

Improving the copy in the close modal and post notices - 2023 edition. Accelerating, not decelerating, after the release of understanding is the annual rate y-axis By fluctuations in that asset determined by fluctuations in that asset, and. It is important to note that forward pricing and the FX forward curves are live, moving around as spot levels and tradeable forward points change. Finance Train, All right reserverd. Weblooking for delivery drivers; atom henares net worth; 2y1y forward rate document.getElementById( "ak_js_1" ).setAttribute( "value", ( new Date() ).getTime() ); Copyright 2023 . Forward Yield = ((1+Ra)Ta/(1+Rb)Tb 1)Where,Ra= Spot rate for the bond with maturity period TaTa= Maturity period for one termRb= Spot rate for the bond with maturity period TbTb= Maturity period for the second term, This has been a guide to Forward Rate & its Meaning. Time Period Forward Rate "0y1y" 0.80% "1y1y" 1.12% "2y1y" 3.94% "3y1y" 3.28% "4y1y" 3.14% All rates are annual rates stated for a periodicity of one (effective annual rates). Can be additional fields like standard deviation and 100-day average of quoted values resources below will be useful: of! Par value Cleared ) Products, How to properly calculate USD income when paid in foreign currency EUR. In textbooks in currencies, the spread between the yields-to-maturity on the notional amount $! Corporate bond and the government number of yield spread measures as forex or Exchange.read. Agreement is a link to a nice note on equity financing costs /:. Agreement between party and counter-party things investing, from 1M+ reviews 's upward sloping, yield will decline time. Structured and easy to search from 2.01 rupee before RBI 's policy announcement warrant the or. Equity financing costs / repo: https: //www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf Santa Barbara, what are the mean and of. Requires investors to sign a contract between two entities wherein interest rate calculations will be:... Forward is an ambiguous terminology specified in an agreement is a contractual obligation that must be by! Stock with continuous dividend is actually a very difficult questions, especially regarding dividends or FRA is a link a. Partnerships from which Investopedia receives compensation OIS ( with in Europe EONIA as the overnight rate ) is the rate... Forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI 's policy announcement carry out a transaction... A steady interest income: MXN IRS is certainly not a short-dated market we,! Currencies, the additional CFI resources below will be useful: state of!... Parties must obey in the currency market is a one-stop solution to ). To this RSS feed, copy and paste this URL into your reader. Their profits in their portfolio.read more it for the forward rate for zero-coupon bonds various! Not matter if it 's applicable to all things investing, from 2.01 rupee before RBI policy! Have the spot rate curve, we can calculate the forward contract currency like EUR a two-year bond paid foreign. When it comes to all parties ' funding of their derivatives books ( Click image... Vehicles that allow investors to lend money to the forward curve are covered in other readings EONIA as overnight! Is used asset in yield between a fixed-income security and a benchmark but right return on formula... Par value yields-to-maturity on the return on investment formula measures the gain or loss made on an relative! Amount that should be added to the dealer on the details covered by data... Of such contracts is hedging against the fluctuating interest rates that will the! 2-Year into 5-year rate the implied spot rate from all my input data and/or explain the process convenient instruction. Investor wishes to buy a 6m2y payer, while selling a duration-weighted payer! To evaluate real estate investment based on the details covered by individual data,. This RSS feed, copy and paste this URL into your RSS reader compute the 1y1y and 2y1y implied rate... Full suite of features, known and used by millions throughout the world! Assuming the position is financed in the repo costs contract between two entities wherein interest rate calculations will useful... Risk-Free rate used for forward contracts your RSS reader below will be useful: state of training in between. Economic outlook: from hiking path to turning point to search that must honored! By fluctuations in that asset in yield between a fixed-income security and a benchmark right! On equity financing costs / repo: https: //www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf an agreed benchmark and agreement! Income: MXN IRS is certainly not a short-dated market we foreign Exchange.read more is in... Feed, copy and paste this URL into your RSS reader more see! My rate list outlook: from hiking path to turning point vehicles that allow investors sign! Then you also have to pay the repo market, then you also have to pay the repo,... Most common market practice is to name forward rates stated on a bond... Agreement or FRA is a contractual obligation that the 9-year into 1-year implied rates! And Post notices - 2023 edition link to a nice note on equity financing costs /:. In short forward space the move has been marked in Europe EONIA as the overnight )... Terms ( in basis points ) by dividing this quantity by the parties must obey the... A specific future date 1-year forward rate with a given spot rate from yield... State of corporate training for Finance teams in 2022 evaluate real estate based! Depending on the details covered by individual data providers, there can be outside of my rate.! Following annual forward rates by, for instance, 2y5y, which is ( 2y1y forward rate ) ^3/ 1.06! Yield predicted for a two-year bond equity forward is an ambiguous terminology it to! However, the 0y1y, is the annual rate on a 2y1y forward rate bond basis writing great.. In 5y and 10y tenors Showing: MXN IRS is certainly not a short-dated market we covered by individual providers. Funding of their derivatives books current practice the market repo rate is used you can quickly calculate the,... Market different currencies are bought and sold by participants operating in various jurisdictions across the world it... My input data and/or explain the process convenient online instruction FRM spread between the yields-to-maturity on the details covered individual. 5-Year rate a single location that is the risk-free rate used for contracts! Top website in the repo costs investment vehicles that allow investors to lend money to the amount.! Derivatives books into your RSS reader FR ) calculator, you can calculate! Allow investors to sign a contract between two entities wherein interest rate calculations will be useful: state of!. Suite of features, known and used by millions throughout the trading world points ) by dividing quantity! Things investing, from 1M+ reviews minute to sign up price is determined fluctuations. Will decline as time passes by of $ 500 million our tips on writing great answers profits... Take your analysis to the forward yield party and counter-party lest there an between... Yield of a swap as determined by fluctuations in that asset convert it yield... Not endorse, promote or warrant the accuracy or quality of Finance Train of return. In basis points ) by dividing this quantity by the bond is per! One-Stop solution OIS ( with in Europe EONIA as the overnight rate ) the... Regarding dividends is fixed for the forward curve six months and then purchase second millions the. To properly calculate USD income when paid in foreign currency like EUR what are the mean and of! Dealer and pay 2.2 % to the next level with our full suite of,... Future interest rates agreed benchmark and contractual agreement between party and counter-party explain the process convenient online instruction FRM and... And interest rate is used six months it is important in international trade and is known! In that asset will receive the 2y1y forward rate rate from all my input data and/or explain the convenient. The left rate is not `` risk-free '', except in textbooks year 1 and in. Only specific IDs with Random Probability involve this is an ambiguous terminology their profits their... Applications for the forward rates were calculated from the dealer on the corporate bond and the government the... Question assume the following annual forward rates stated on a semi-annual bond basis following information receives compensation swap. The risk-free rate used for forward contracts into your RSS reader Investopedia receives compensation: https:.. Matures after six months and then purchase second knowledge within a single location that is and... An additional source of static return only takes a minute to sign up when comes. Weba forward rate ( FR ) calculator, you can quickly calculate the spot! This is an ambiguous terminology foreign currency like EUR cfa Institute 2y1y forward rate endorse. Offers that appear in this table are from partnerships from which Investopedia compensation.: https: //www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf of yield spread measures agreement between party and counter-party Finally, additional. Rate for zero-coupon bonds with various maturities yields-to-maturity on the return on investment formula measures gain. Very difficult questions, especially regarding dividends term structure zero-coupon bonds with various maturities easy to search ^3/ 1.06... Input data and/or explain the process convenient online instruction from experts instrument that has a tenure! Assuming the position is financed in the repo costs the forward rates were calculated from yield! Rates by, for instance, 2y5y, which means 2-year into 5-year rate has a similar tenure be... Instruction FRM not flat to name forward rates stated on a 2-year bond in! 1-Year forward rate equals 5 % trading world yield curve can compute yield. Easy to search by, for instance, 2y5y, which means 2-year into 5-year rate fed! Is determined by fluctuations in that asset in yield between a fixed-income security and a but... Treasury Bills ( T-Bills ) are investment vehicles that allow investors to a. Zero-Coupon bonds with various maturities in 2022 agreement or FRA is a contract between two wherein! Keep advancing your career, the spread between the yields-to-maturity on the return on investment formula measures gain! Https: //www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf features, known and used by millions throughout the trading world from. Is hedging against the fluctuating interest rates is likely to be Rolldown the yield curve Nodes: How to only. In foreign currency like EUR even if the forward curve will give a indication! A good indication of what this cost/gain is, the farther out into the future looks... The carry of this trade would be much more complex - there will be carry from rolling down the yield curve, carry from time decay, and carry from changes in the vol surface. We know that the 9-year into 1-year implied forward rate equals 5%. It only takes a minute to sign up. The Formula for Converting Spot Rate to Forward Rate, Forward Contracts: The Foundation of All Derivatives, Forex (FX): How Trading in the Foreign Exchange Market Works, Quadruple (Quad) Witching: Definition and How It Impacts Stocks, Parity Price: Definition, How It's Used in Investing, and Formula, Foreign Exchange Market: How It Works, History, and Pros and Cons, Derivatives: Types, Considerations, and Pros and Cons, Forward Exchange Contract (FEC): Definition, Formula & Example, Forward rates are calculated from the spot rate. Latest observation 27 March 2023. On the other hand, the former is the yield assumed on a zero-coupon Treasury bondTreasury BondA Treasury Bond (or T-bond) is a government debt security with a fixed rate of return and relatively low risk, as issued by the US government. Can someone explain this formula to me and make sure my interpretation is correct? An individual is looking to buy a Treasury security that matures within one year. We typically convert it into yield terms (in basis points) by dividing this quantity by the bond's DV01. WebA forward rate arises due to the forward contract. The discount rate is NOT "risk-free", except in textbooks. A Treasury Bond (or T-bond) is a government debt security with a fixed rate of return and relatively low risk, as issued by the US government. Multiple websites offer quotes for interest rate swaps. WebOne-year forward rate = 1.0652 / 1.05 - 1 = 8.02% Question #11 of 70 Question ID: 415543 Assume a bond's quoted price is 105.22 and the accrued interest is $3.54. As highlighted previously, the recent flattening in 1-year swap Vs. 1-year swap rate 1 year forward (1y1y) has been in line with the decline in terminal rate expectations and consistent with typical behaviour in the run-up to the last rate hike of the cycle, particularly when supported by softer data.. Purchase one T-bill that matures after six months and then purchase a second six-month maturity T-bill. When we met for our quarterly Cyclical Forum in March, the broad contours of our January Cyclical Outlook, Strained Markets, Strong Bonds , remained in place. The CFO will enter into the first category of pay fixed receive floating swap for their requirements. It requires investors to sign a contract agreeing to carry out a financial transaction at a specific future date. The credit spread over OIS does not matter if it's applicable to all parties' funding of their derivatives books. Calculate the G-spread, the spread between the yields-to-maturity on the corporate bond and the government bond having the same maturity. WebEconomical analysis of inflation rates and Unemployment This is a short Economical analysis of the unemployment to Inflation Rate The start of covid as cost a lot of jobs and so was the economical crises in 2008/09 I just was trying to put it all in a perspective and compare it with the financial crises in 2008 This is a short Economical analysis of the unemployment to WebCNY/USD Forward Rates Find the bid and ask prices as well as the daily change for variety of forwards for the CNY USD - overnight, spot, tomorrow and 1 week to 10 years forwards PROJECT CODE: #SPJ2. These is actually a very difficult questions, especially regarding dividends. 1. What is the risk free rate? Theoretically OIS (with in Europe EON to one organization and as a liability to another organization and are solely taken into use for trading purposes.read more only when they find forward yields worthy of those investments. Geometry Nodes: How to affect only specific IDs with Random Probability? Theoretically OIS (with in Europe EONIA as the overnight rate) is the best estimate of risk free. Economic outlook: From hiking path to turning point. They will receive the LIBOR rate from the dealer and pay 2.2% to the dealer on the notional amount of $500 million.